JLL summarizes 2015's industrial market in Poland

- 2015 saw over 2.2 million sq m of industrial space leased in Poland .

- Due to high tenant activity, the vacancy rate dropped to 6.2%.

- Nearly 1 million sq m of warehouse space was delivered to the market while a further 774,000 sq m is under construction.

- 35% of space under construction is speculative

Advisory firm JLL summarizes 2015's industrial market in Poland.

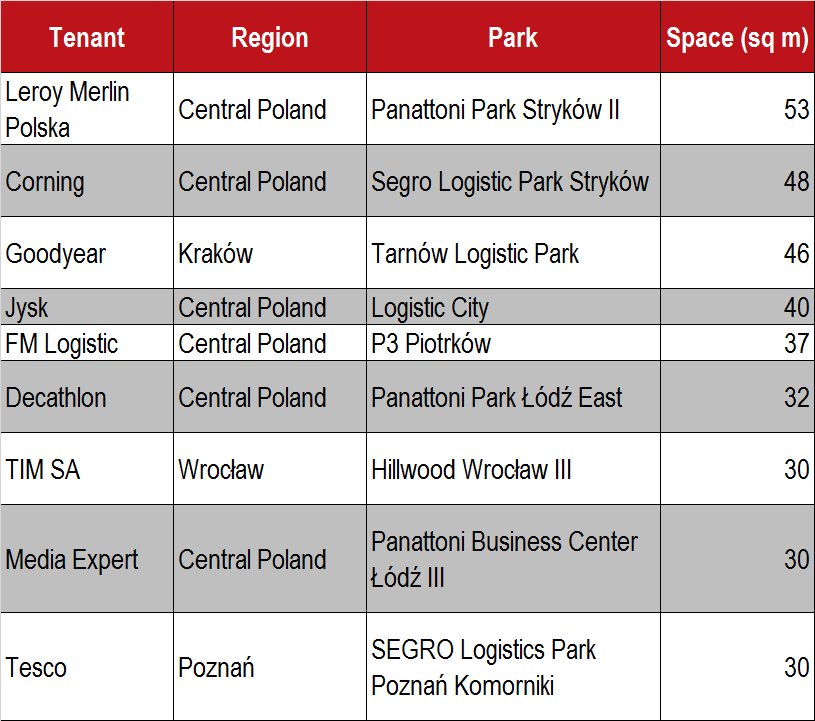

Tomasz Olszewski, Head of Industrial CEE at JLL, says: “The industrial market in Poland continued to be buoyant in 2015. Gross take-up reached a historically record-breaking total of over 2.2 million sq m. Central Poland saw the highest volume of leased space – 527,000 sq m, while Warsaw’s Suburbs recorded 409,000 sq m followed by Upper Silesia region with 359,000 sq m. The largest deal was signed by Leroy Merlin – 53,000 sq m in Panattoni Park Stryków II”.

Net take-up totaled a strong 1.47 million sq m. This is the market's best performance since 2008's record-breaking volume of 1.55 million sq m.

Selected industrial lease transactions in 2015

Source: JLL, www.warehousefinder.pl, Q4 2015

The biggest demand for warehouse space in 2015 came from logistics operators and retailers (a 34.7% and 17.9% share in gross take-up respectively).

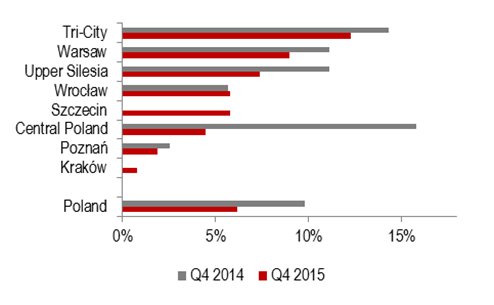

Vacancy rate drops

The vacancy rate had been dropping throughout the year and hit 6.2% by the end of 2015. According to www.warehousefinder.pl, the huge take-up in Central Poland resulted in a decrease in vacancy rates from 15.8% to 4.6% in this region.

Vacancy rate by region in Q4 2014 vs Q4 2015 (%)

Source: JLL, www.warehousefinder.pl, Q4 2015

Supply

At the end of 2015, the total stock on the Polish industrial market stood at 9.77 million sq m. The major markets include Warsaw (approx. 2.9 million sq m within Warsaw Inner City and Suburbs), Upper Silesia (1,7 million sq m), Poznań (1.6 million sq m), Central Poland (1.3 million sq m) and Wrocław (1.3 million sq m).

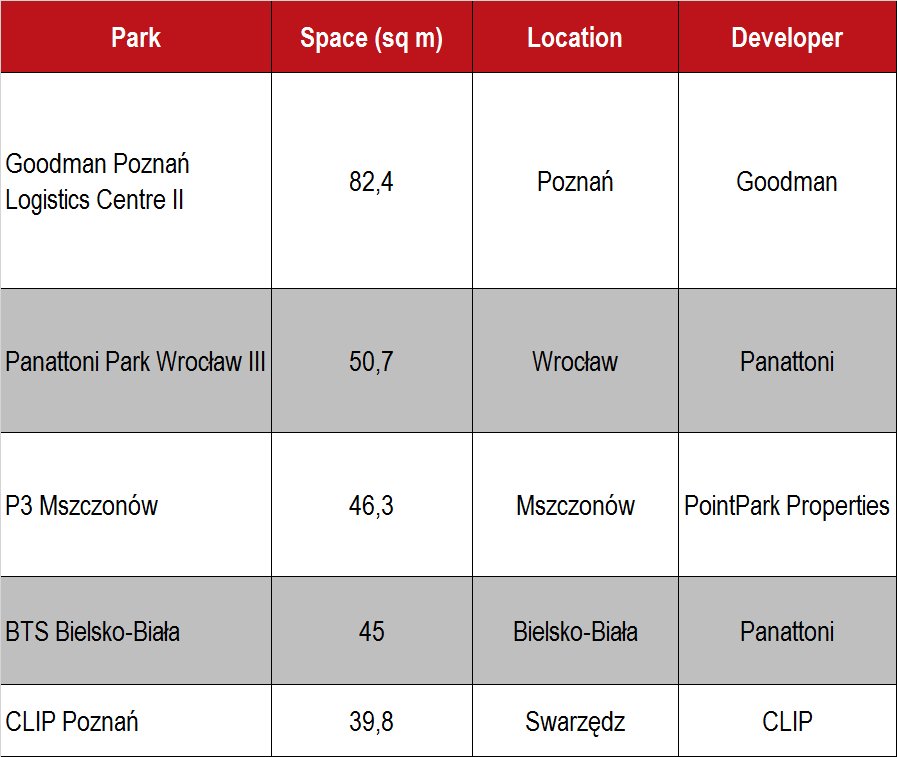

During the year, the market grew by nearly 1 million sq m, with a large proportion of this number down to Panattoni (443,000 sq m), Goodman (222,000 sq m) and SEGRO (87,000 sq m). Poznań managed to deliver the largest supply totaling 278,000 sq m, followed by Upper Silesia region with 140,000 sq m and Wrocław- 108,500 sq m. Furthermore, excellent results in terms of new supply were also recorded in smaller locations such as Szczecin (70,000 sq m), Rzeszów (60,500 sq m) and Lublin (59,000 sq m).

Largest completions in 2015

Source: JLL, www.warehousefinder.pl, Q4 2015

“As of the end of 2015, some 774,000 sq m of modern warehouse space was under construction in 33 projects across Poland. Warsaw Suburbs topped the list of regions, with nearly 219,000 sq m in the construction stage at the end of 2015. 35% of space under construction is speculative – without binding lease agreements - which indicates that developers have put a great deal of trust in Poland and recognize the excellent opportunities for further development of the country's industrial market,” adds Tomasz Olszewski.

Panattoni is way ahead of its competitors, as its total amount of space under construction currently stands at 567,000 sq m, which is 73% of all stock in the pipeline.

Rents

Headline rents in smaller SBU units (located within city boundaries and characterized by higher rent levels compared to large distribution parks) are between €3.50 and €4.00 / sq m / month in Wrocław and €3.40 and €4.30 / sq m / month in Łódź (Central Poland).

Headline rents in big box units are diversified by region and are at €2.60 –€ 3.20 / sq m / month in Central Poland or €3.,80 - €4.50 / sq m / month in Kraków. The highest levels are to be found in Warsaw Inner City, and are between €4.10 and €5.30 / sq m / month.

Effective rents (including incentives from owners) within industrial parks are also influenced by region, with the lowest levels of between €1.90 and €3.10 / sq m / month in Upper Silesia and the highest in Warsaw Inner City, ranging from €3.50 to €4.80 / sq m / month.

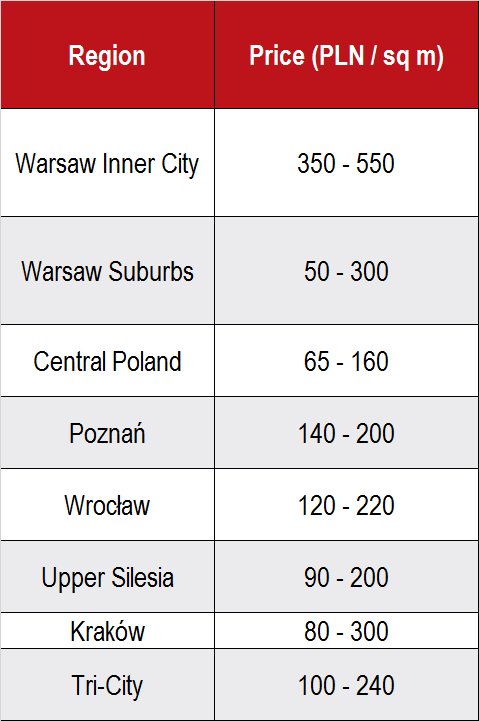

Industrial land

Agata Zając, Associate Director, Industrial, JLL, comments: “After the successful development of projects in smaller cities, developers continue their search for interesting industrial sites in locations such as Szczecin, Bydgoszcz, Lublin and Rzeszów. There is still huge interest in Warsaw, especially in its western and southern districts, due to the A2 motorway, the S8 route and the planned S7 route. Intensive searches for new investment land are also being carried out in Łódź and adjacent areas, particularly those in close proximity to the A1 motorway. Traditionally, the main focus is on well- located sites, in the vicinity and with convenient access to major transport nodes.”

Throughout the year land prices remained stable in all major markets. A small increase in Tri-City's upper band was recorded in Q4 2015 (from PLN 200 to PLN 240 /sq m).

Source: JLL, www.warehousefinder.pl, Q4 2015

It is worth highlighting that recent legislative changes regarding land acquisition proposed by the new government might significantly restrict the development process from May 2016 onwards. These changes will certainly have a negative impact on warehouse developers, by adding stricter conditions regarding the change of land use, namely from agricultural to developable land.

Investment market

Tomasz Puch, Head of Office and Industrial Investment at JLL, says: “In 2015, the industrial investment market reported €473 million in 14 transactions. According to our research, a significant share - 36% - of the industrial investment volume was attributed to sale-and-lease-back transactions, while portfolio deals accounted for more than 75%. Throughout 2015, we registered further prime yield compression to a level of below 7.00% for the best-located, long-term leased strategic assets.”

Tomasz Puch, Head of Office and Industrial Investment at JLL, says: “In 2015, the industrial investment market reported €473 million in 14 transactions. According to our research, a significant share - 36% - of the industrial investment volume was attributed to sale-and-lease-back transactions, while portfolio deals accounted for more than 75%. Throughout 2015, we registered further prime yield compression to a level of below 7.00% for the best-located, long-term leased strategic assets.”

Selected industrial investment transactions in Poland (2015)

Source: JLL, www.warehousefinder.pl, Q4 2015

Over 57% of industrial space in Poland is in the hands of five key market players (Prologis, SEGRO, Blackstone/Logicor, Goodman and Panattoni) and their JV Partners.

“In 2016, we might expect an increase in investor activity and transaction volumes as well as a further yield compression”, adds Tomasz Puch.

Forecasts

“In 2016, the modern industrial stock will exceed 10 million sq m. We expect further development of smaller markets such as Lublin, Rzeszów, Tri-City and Szczecin, which will be encouraged by improvements in road infrastructure. Eastern Poland - especially Białystok, as well as Kielce are new locations with development potential. Furthermore, it is worth adding that the industrial market quickly responds to changes in economic conditions and depends on the situation in other countries. International factors that are the challenges for this year include the signs of economic slowdown in China and USA, the unstable political situation in the Ukraine as well as discussions regarding potential changes to the Schengen zone. Nevertheless, it is worth noting that the industrial market is mostly dependent on the Polish economy which to date has fared well. Assuming that there are no changes to the economic fundamentals of both Poland’s economy and the international environment, we do not anticipate the recent growth dynamics to weaken in the near future”, adds Tomasz Olszewski.

JLL